Cyber Insurance Denied Claims: The Common Reasons

Why do cyber insurance claims get denied? The recurring reasons, from misrepresented controls to war exclusions, and how to avoid each one before you file.

A denied cyber insurance claim is the worst possible time to learn how your policy actually works. You’ve had the incident, you’ve absorbed the cost, and now the carrier is explaining why the coverage you paid for doesn’t apply. Most of these denials are not surprises in hindsight. They fall into a handful of recurring categories, and nearly all of them are visible before you ever file.

Having sat on the buyer’s side of these programs, the pattern is consistent: claims get denied for reasons the organization could have seen coming. Here are the ones that come up again and again, and what to do about each before it costs you.

Why do cyber insurance claims get denied?

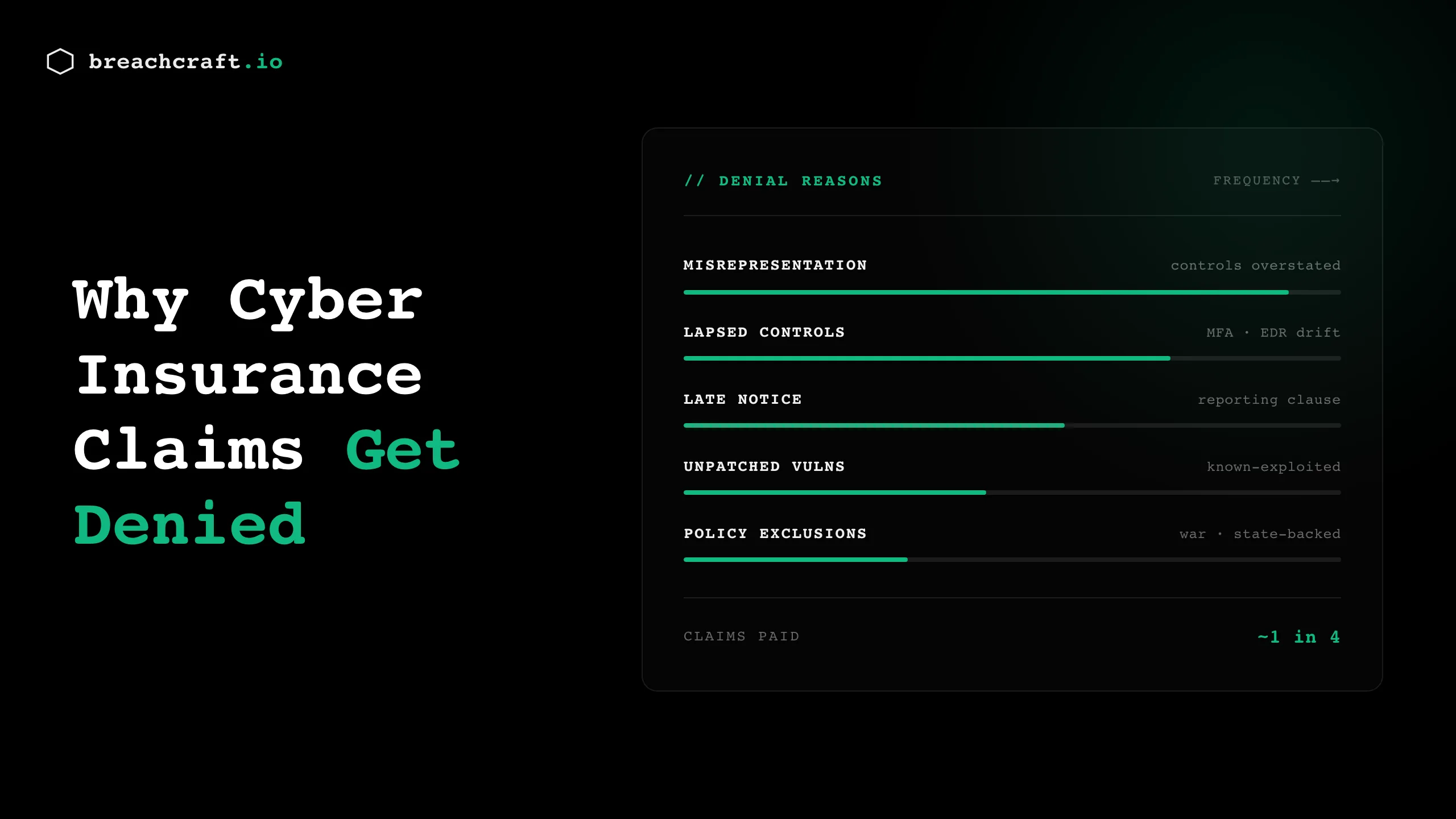

Cyber claims are most often denied for misrepresentation on the application (attesting to controls you didn’t fully have), failure to maintain those controls after the policy binds, late notice that breaches the reporting clause, or a loss that falls under a policy exclusion such as a state-backed cyberattack. The NAIC’s 2025 report shows only about 1 in 4 closed cyber claims resulted in a payout, though not all of those were formal denials. The common thread among the denials that are preventable is a gap between what you told the carrier and what was actually true when the incident happened.

Misrepresentation on the application

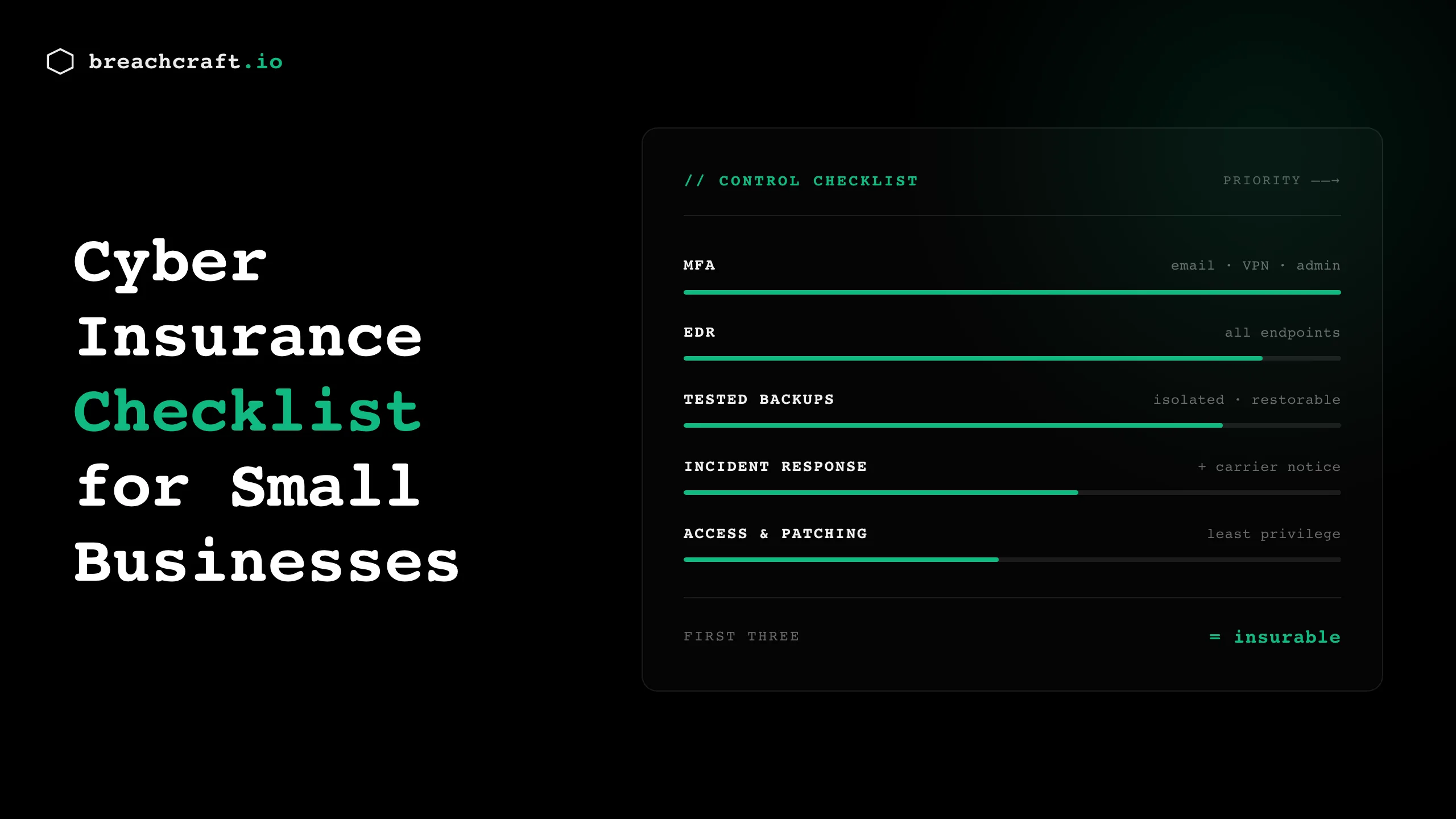

This is the big one. Modern cyber applications are detailed, and you attest to specific controls: MFA everywhere, endpoint detection and response, tested backups, an incident response plan. If any of those attestations overstate reality, the carrier has grounds to deny a related claim and, in some cases, rescind the policy from inception.

The trap is rarely deliberate fraud. It’s the well-meaning “yes” to “do you enforce MFA across your environment?” when MFA covers email but not the VPN, or covers employees but not the service accounts running your critical systems. At claim time, the carrier’s forensics will establish how the attacker got in. If the answer is a path you attested was protected, the gap between the application and reality becomes the denial.

How to avoid it: answer the application against what you can prove, not what you intend to finish. A gap assessment that maps your real controls to the specific questions carriers ask surfaces these mismatches before you sign the application, not after the breach.

Failure to maintain the controls you attested to

Some organizations get the application right and then drift. MFA gets disabled on a system during a migration and never re-enabled. An EDR agent falls off a segment of endpoints. A backup job silently fails for months. The application was accurate the day you signed it, but the control lapsed before the incident.

Many policies treat continuous control maintenance as a condition of coverage. When a claim traces back to a control you attested to but let lapse, the carrier can deny on those grounds. This is the category that catches mature organizations, because the initial application was honest; the failure was operational drift over the policy year.

How to avoid it: treat your attestations as ongoing commitments. Monitor the controls carriers care about the way you’d monitor any production system, and fix drift quickly. Ongoing security leadership, whether internal or a virtual CISO, is often what keeps attested controls from quietly decaying between renewals.

MFA gaps, specifically

MFA deserves its own category because it’s the single most common control gap behind denials. Carriers have moved past accepting “we have MFA” and now ask whether it’s applied everywhere and whether it’s phishing-resistant for privileged access. The classic gap is partial coverage: strong MFA on the front door, nothing on a side entrance the attacker actually used.

Service accounts are the blind spot within the blind spot. They can’t use interactive MFA, so they need equivalent controls: rotation, vaulting, least privilege, monitoring. Leaving them with static passwords and broad rights recreates exactly the exposure MFA was supposed to close, and carriers increasingly ask about it directly.

How to avoid it: inventory every authentication path, not just the obvious ones, and confirm MFA or an equivalent control covers each. Our cyber insurance requirements guide breaks down what carriers expect from MFA in detail.

Late notice and the reporting clause

Cyber policies carry notification requirements, and they’re stricter than many buyers realize. Report the incident outside the window your policy specifies, or handle it internally before looping in the carrier, and you can breach a condition of coverage. Organizations that try to quietly resolve an incident first, then file once they realize the cost, sometimes find they’ve forfeited the claim by waiting.

How to avoid it: know your notice window before you have an incident, and build carrier notification into your incident response plan as an early step. When in doubt, notify. A precautionary notice rarely hurts you; a late one can end the claim.

Failure to patch known-exploited vulnerabilities

If an attacker walks in through a vulnerability that had a patch available for months, some carriers will scrutinize whether your patching program met the standard you attested to. Exploitation of a long-known, unpatched flaw can shift a claim from “unfortunate incident” to “failure to maintain reasonable security,” depending on the policy and the facts.

How to avoid it: run a real vulnerability management program with defined timelines for critical patches, and document it. Carriers want evidence of a functioning process that closes known-exploited flaws on a schedule, and a documented one clears the bar even when it isn’t perfect.

Policy exclusions, including state-backed cyberattacks

Some denials have nothing to do with your controls; they come down to what the policy excludes. The most consequential recent development is the war and state-backed cyberattack exclusion. After the NotPetya attack in 2017, insurers invoked “act of war” language to deny large claims. In the landmark dispute, Merck held a $1.75 billion all-risk policy and its insurer denied a NotPetya claim under the war exclusion; courts sided with Merck, finding the exclusion written for traditional warfare didn’t apply to a cyberattack, and the parties settled confidentially, leaving no definitive case law.

The industry’s response was to rewrite the language. Lloyd’s of London required state-backed cyberattack exclusions on its cyber policies from March 31, 2023. So current policies increasingly carry explicit exclusions for attacks attributed to nation-states, particularly those that significantly impair a state’s function or security. Attribution is contested and slow, which makes this a real coverage risk for exactly the kind of sophisticated attack you’d most want covered.

How to avoid it: you can’t control geopolitics, but you can read the exclusion. Before you buy, understand your policy’s war and state-backed language, how attribution is defined, and whether any carve-backs exist. This is a conversation to have with your broker at placement, not after an incident gets attributed to a foreign actor.

Retroactive dates and the policy period

Cyber policies cover incidents within a defined period, and claims-made policies add a retroactive date: incidents before that date aren’t covered even if you discover them later. Organizations that switch carriers or let coverage lapse and rebind can create gaps where an incident falls outside every policy’s window. A breach that started before your retroactive date, or surfaced during a lapse, can be denied on timing alone.

How to avoid it: manage continuity at renewal. Watch your retroactive date when you change carriers, avoid coverage gaps, and understand that dwell time matters. Attackers often sit in an environment for months, so the date an incident “began” may predate the date you found it.

The through-line

Look across these categories and the pattern is clear. A few denials are structural (exclusions, timing) and the rest come down to the gap between what you attested and what was true. The controllable ones are, in a sense, good news: they mean the outcome is largely in your hands before you ever file.

The single most effective move is making sure your application is accurate and your controls stay that way. If you’re not certain where your program stands against what carriers will ask, a gap assessment maps it before you sign, and understanding how penetration testing affects your premiums rounds out what carriers expect at higher coverage tiers. Both beat discovering the gap the hard way.

Preparing for a renewal or worried your controls won’t hold up under a claim? Contact Breach Craft and we’ll help you close the gaps carriers actually check.