How Penetration Testing Affects Cyber Insurance Premiums

Does a pentest lower your cyber insurance premium? Usually not as a discount. Here's how testing actually affects eligibility, sub-limits, and renewal.

There’s a common belief that a penetration test buys you a cheaper cyber insurance premium, the way a home security system trims your homeowner’s policy. It’s a reasonable assumption. It’s also mostly wrong, and acting on it can leave you disappointed at renewal.

Testing does affect your insurance, sometimes significantly. But the effect rarely shows up as a line-item discount. It shows up in whether you qualify for the coverage you want, what sub-limits the carrier attaches, and whether a claim gets paid when you need it. Here’s how underwriters actually use pentest results, and where testing moves real money.

Does penetration testing lower cyber insurance premiums?

Not usually as a direct discount. Carriers price cyber policies on demonstrated control maturity, and a penetration test is one of the strongest ways to prove yours. The bigger effect is on eligibility and terms: a current, well-scoped test with remediation evidence keeps you eligible for higher coverage limits, helps you avoid surcharges applied to weak applicants, and can restore ransomware sub-limits that carriers cut for organizations that can’t demonstrate testing. Skip it above certain coverage thresholds and you may not get the policy at all, or you’ll get it with limits and exclusions that make it far less useful. So the honest framing isn’t “test and pay less.” It’s “test and stay insurable on terms you can live with.”

Underwriters use pentest results as a gate, not a coupon

Cyber underwriting has changed. A few years ago, an application was mostly a checklist you attested to. Today, for any meaningful coverage, the carrier wants evidence, and the penetration test is a primary piece of it.

What the underwriter is doing with your report is risk selection. They’re deciding whether to write your policy at all, and if so, at what limit and price. A strong report signals a mature program and puts you in a better risk pool. A missing report, or a stale one, pushes you toward the applicants the carrier would rather not write, and that’s where the money moves against you.

This is why the “discount” mental model breaks down. You’re not earning points off a sticker price. You’re establishing which tier of applicant you are. The organizations that test well don’t get a coupon; they get access to better limits and cleaner terms than the organizations that don’t.

Where testing actually moves money

If the effect isn’t a straightforward premium cut, where does it show up? Three places, in order of how often we see them matter.

Eligibility for the coverage limit you need. Most carriers have an informal threshold, often around $1M in coverage, where testing shifts from recommended to required, and it’s nearly universal above $5M. Below that line you might get coverage without a test. Above it, the test is what unlocks the limit. An organization that wants $5M in coverage but can’t produce a current pentest often gets offered $1M or $2M instead, if anything. That gap is the real cost, and it dwarfs any premium percentage.

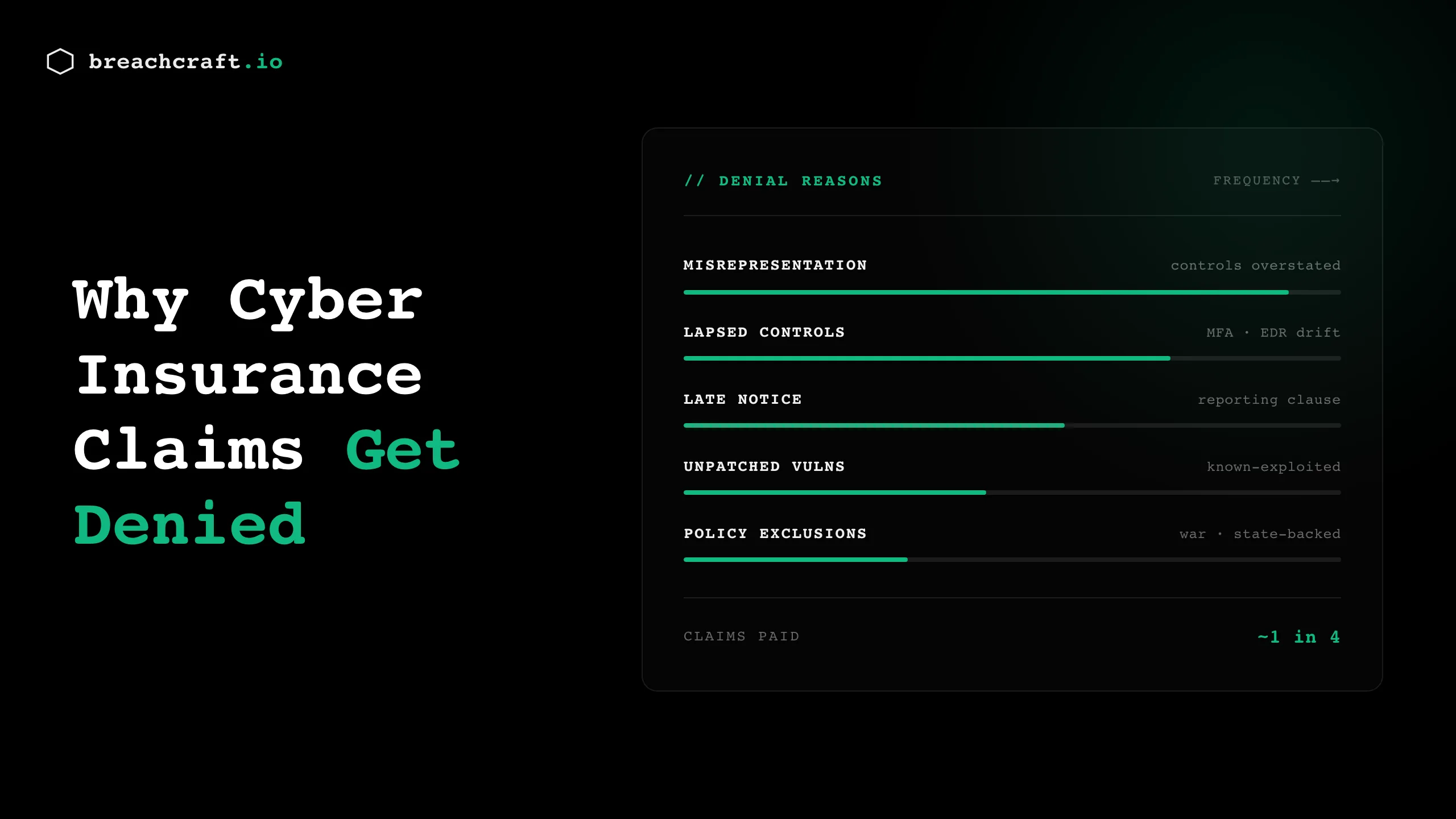

Sub-limit restoration, especially ransomware. After the ransomware loss years, carriers started attaching sub-limits: your policy might be $5M overall but cap ransomware payouts at $1M unless you demonstrate specific controls. Penetration testing that validates your segmentation, backup isolation, and privileged-access controls is often part of what gets that sub-limit restored toward the full policy amount. Coalition’s 2026 Cyber Claims Report found that 70% of 2025 ransomware events involved both encryption and data exfiltration, often doubling the incident cost, which is exactly why carriers scrutinize these controls before restoring a ransomware sub-limit. Restoring it keeps a ransomware event from becoming a mostly-uncovered loss, which is worth far more to you than any premium line-item.

Surcharge avoidance. Carriers apply loadings to applications that look risky. A weak or absent testing story is one of the flags. You rarely see a “we tested” credit itemized on the quote, but you feel the absence of a surcharge that a comparable untested applicant pays. It nets out in your favor without ever appearing as a discount.

None of this shows up cleanly on the quote as “penetration testing: minus X percent.” It shows up as a better limit, a restored sub-limit, and the surcharge you didn’t pay.

What the report has to show to count

A test only helps if the report holds up under an underwriter’s review. The cyber insurance requirements carriers publish are getting specific about this, and a report that just proves a test happened isn’t enough.

At larger coverage tiers, underwriters want to see:

- The methodology and scope (black-box, gray-box, or white-box, and what was in bounds)

- Findings with severity ratings

- Evidence that critical and high findings were remediated

- A retest confirming the criticals were actually closed

The pattern that fails is a clean-looking report against a limited scope. We’ve seen organizations test five servers in a 200-server environment and present the tidy result. Carriers are getting better at catching this, and a scope that doesn’t match your real footprint is worse than no test, because it edges into misrepresentation. Scope your penetration test to your actual environment, fix the criticals, and keep the remediation record. That record is what underwriting actually scores.

Why the scan on your application won’t do it

Cyber applications often ask whether you conduct “regular vulnerability scanning or penetration testing,” and the wording tempts organizations to satisfy it with the cheaper option. At higher coverage levels, that doesn’t hold.

A vulnerability assessment uses automated tooling and manual review to list what’s exposed. A penetration test attempts to exploit those weaknesses, chain them, and demonstrate real impact. For insurance above $1M, and almost universally above $5M, carriers want the pentest, because it answers the question they care about: not “what’s exposed” but “what could an attacker actually do here.” If you’re unsure which one your policy requires, the distinction is worth understanding before you apply. Our breakdown of penetration testing versus vulnerability assessment covers where each one fits.

Time the test to your renewal, not your calendar

Most organizations don’t skip the test; they run it too late to matter. A pentest completed the week before renewal proves you tested. It doesn’t prove you fixed anything, and remediation evidence is the part underwriters weight most heavily.

Work backward from your renewal date. If you renew in November, a September test leaves room to remediate the criticals and produce a retest showing they’re closed. That sequence, test then fix then retest, is what turns a report into a strong position at renewal instead of a box you checked. If you’re not sure where your program stands against what carriers will ask for, a gap assessment maps it before you’re mid-application.

The part most people miss: testing protects the claim, not just the premium

Premiums get the attention because you pay them every year. The claim is where the policy actually earns its keep, and that’s where a testing record quietly does its most important work.

When you file a cyber claim, the carrier’s first move is to confirm the controls you attested to were real. If your application said you conducted annual penetration testing and remediated critical findings, the adjuster may ask you to prove it. An organization that can produce dated reports and retest evidence is on solid ground. One that attested to a testing program it didn’t actually run is exposed, because carriers can deny claims, and in some cases rescind coverage retroactively, when the application doesn’t match reality.

This is not a hypothetical. That same Coalition report found that 64% of 2025 claims closed with no out-of-pocket loss for the policyholder, which is what coverage looks like when the controls behind the application are real. The organizations that get burned are the ones whose attestations don’t hold up: carriers can deny a claim, and in some cases rescind coverage retroactively, when the security controls you signed for weren’t actually in place. Testing is how you stay out of that group. The report you file at renewal is also the evidence that backs your claim if the worst happens, which is another reason a real, well-scoped test beats a cosmetic one. A cheap test that overstates your posture doesn’t just weaken your renewal; it can undercut the payout you’re counting on.

Put plainly: the premium is what testing helps you manage in a good year. The claim is what testing helps you protect in a bad one. Both arguments point at the same practice, done properly.

How Breach Craft approaches insurance-driven testing

When testing is tied to an insurance renewal, the deliverable matters as much as the test. We scope engagements to match your real environment rather than a convenient subset, rate findings so an underwriter can read them, and provide the retest documentation that proves criticals were closed. We’ve received hundreds of these reports from the other side of the table over the years, so we write them for the audience that reviews them: your underwriter, your broker, and your own leadership.

The goal is a report that holds up when a carrier’s technical reviewer reads it closely. That is what protects both your terms at renewal and your claim if you ever have to file one.

Preparing for a renewal or trying to qualify for higher limits? Contact Breach Craft to scope a penetration test built for how carriers actually evaluate them.