Cyber Insurance vs Cyber Liability Insurance

Cyber insurance vs cyber liability: the real distinction is first-party vs third-party coverage. What each protects, how they're packaged, and where gaps hide.

“Cyber insurance” and “cyber liability insurance” get used as if they mean the same thing, and in casual conversation they mostly do. But when you’re actually buying coverage or filing a claim, the loose terminology hides a distinction that matters: what the policy covers your own losses versus what it covers when other people come after you. Understanding that split is what keeps you from buying a policy that only covers half your incident.

What’s the difference between cyber insurance and cyber liability insurance?

In practice, the two terms are used interchangeably, and most modern policies bundle both. The distinction that actually matters is first-party versus third-party coverage. First-party coverage pays for your own losses from an incident: forensics, data restoration, business interruption, ransomware costs, and breach notification. Third-party coverage, which is the true “liability” piece, pays for claims others bring against you: lawsuits from affected customers, regulatory fines, and contractual penalties. A complete cyber policy includes both. So the useful question is whether a policy covers both your direct losses and your liability to others, because a single incident usually creates both.

First-party coverage: your own losses

First-party coverage responds to the costs your organization absorbs directly when an incident hits. This is the part people picture when they imagine “cyber insurance,” even though the name doesn’t say so. It typically includes:

- Incident response and forensics. The cost of investigators to determine what happened and contain it.

- Data and systems restoration. Rebuilding systems and recovering data after an attack.

- Business interruption. Lost income while you’re down, which for many organizations is the largest single cost of a cyber event.

- Ransomware and extortion. Ransom payments where legal and covered, plus the response costs around them.

- Breach notification. The expense of notifying affected individuals and regulators, often a legal requirement with tight timelines.

If your bigger exposure is operational (an attack that stops you from operating), first-party coverage is what you’ll lean on. Ransomware is the clearest example: it’s overwhelmingly a first-party loss, which is why a policy that’s strong on liability but thin on first-party coverage can leave you badly exposed to the most common serious incident.

Third-party coverage: what you owe others

Third-party coverage, the genuine “liability” component, responds when someone else suffers because of your incident and comes to you for it. If you hold other people’s data (customers, patients, partners), this is where your exposure concentrates. It typically covers:

- Privacy liability. Claims from individuals whose data you exposed.

- Regulatory defense and fines. The cost of responding to a regulator and, where insurable, the penalties. This matters under regimes with real teeth, and understanding your obligations under frameworks like HIPAA or state privacy laws shapes how much of this coverage you need.

- Media and content liability. Claims arising from your digital content.

- Contractual and PCI penalties. Fines and assessments tied to agreements or payment-card standards.

An organization that holds large volumes of sensitive personal data has more third-party exposure than one that doesn’t. A healthcare provider or a business handling payment cards feels this side of the policy most.

One incident, both sides of the policy

The distinction matters because a single event rarely stays on one side. Picture a ransomware attack on a small healthcare billing company. The immediate costs are first-party: forensics to scope the breach, restoring encrypted systems, and lost revenue during the days the business can’t process claims. But the same attack exfiltrated patient records, which triggers the third-party side: notification obligations, potential regulatory action under HIPAA, and lawsuits from patients whose data was exposed.

One incident, two very different sets of costs. A policy missing either side leaves a hole exactly where you’d feel it. This is why “do I need first-party or third-party” is usually the wrong question. Most organizations need both, because most serious incidents produce both.

How they’re packaged, and where gaps hide

Most cyber policies sold today bundle first-party and third-party coverage, which is part of why the terminology blurred in the first place. But bundled doesn’t mean equal. The coverage amounts, sub-limits, and conditions differ across the components, and that’s where gaps live.

The one to watch most closely is sub-limits. Your policy might carry a $5 million overall limit but cap ransomware or business interruption at a fraction of that unless you demonstrate specific controls. A policy can look complete on the declarations page and still leave your most likely loss under-covered. Read the sub-limits, not just the headline number, and read the exclusions, which increasingly include war and state-backed cyberattack language that can remove coverage for sophisticated attacks.

There’s a second structural detail worth checking: whether first-party and third-party coverage share a single limit or carry separate ones. If they share a $2 million limit, a large first-party loss can erode what’s left for a third-party claim arising from the same event, and the reverse is equally true. Separate limits cost more, but they protect you in exactly the scenario above, where one incident hits both sides at once and a shared limit runs out before the second set of costs is covered.

The practical review: confirm the policy has both first-party and third-party coverage, check the sub-limits on the losses most likely to hit you, and understand the exclusions and the control conditions attached to each piece. A policy that’s strong where your risk isn’t, and thin where it is, is a common and avoidable mistake.

Questions worth asking before you buy

You don’t need to be an insurance expert to buy well. You need a broker who’ll answer a handful of plain questions, and enough clarity about your own risk to know which answers matter most:

- Does this policy include both first-party and third-party coverage, or only one?

- Are the limits shared or separate across the two?

- What are the sub-limits on ransomware and business interruption, and what controls keep them intact?

- What does the war and state-backed cyberattack exclusion say, and how is attribution defined?

- Does the regulatory defense and fines coverage apply to the frameworks I’m actually subject to?

If a broker can’t answer these clearly, that’s information too. The questions exist to make sure the policy you buy matches the incidents you’re actually likely to face.

Matching coverage to your actual risk

The right balance depends on your organization. A data-heavy business (lots of customer or patient records) leans toward third-party exposure and should scrutinize privacy liability and regulatory coverage. An operations-heavy business (where downtime is the killer) leans first-party and should focus on business interruption and ransomware limits. Most organizations need meaningful coverage on both sides, but the emphasis shifts.

Knowing which side matters more starts with understanding your own risk, and that’s where a security assessment pays off before you ever talk to a broker. A gap assessment clarifies where your exposure actually concentrates, which in turn tells you where your policy needs to be strongest.

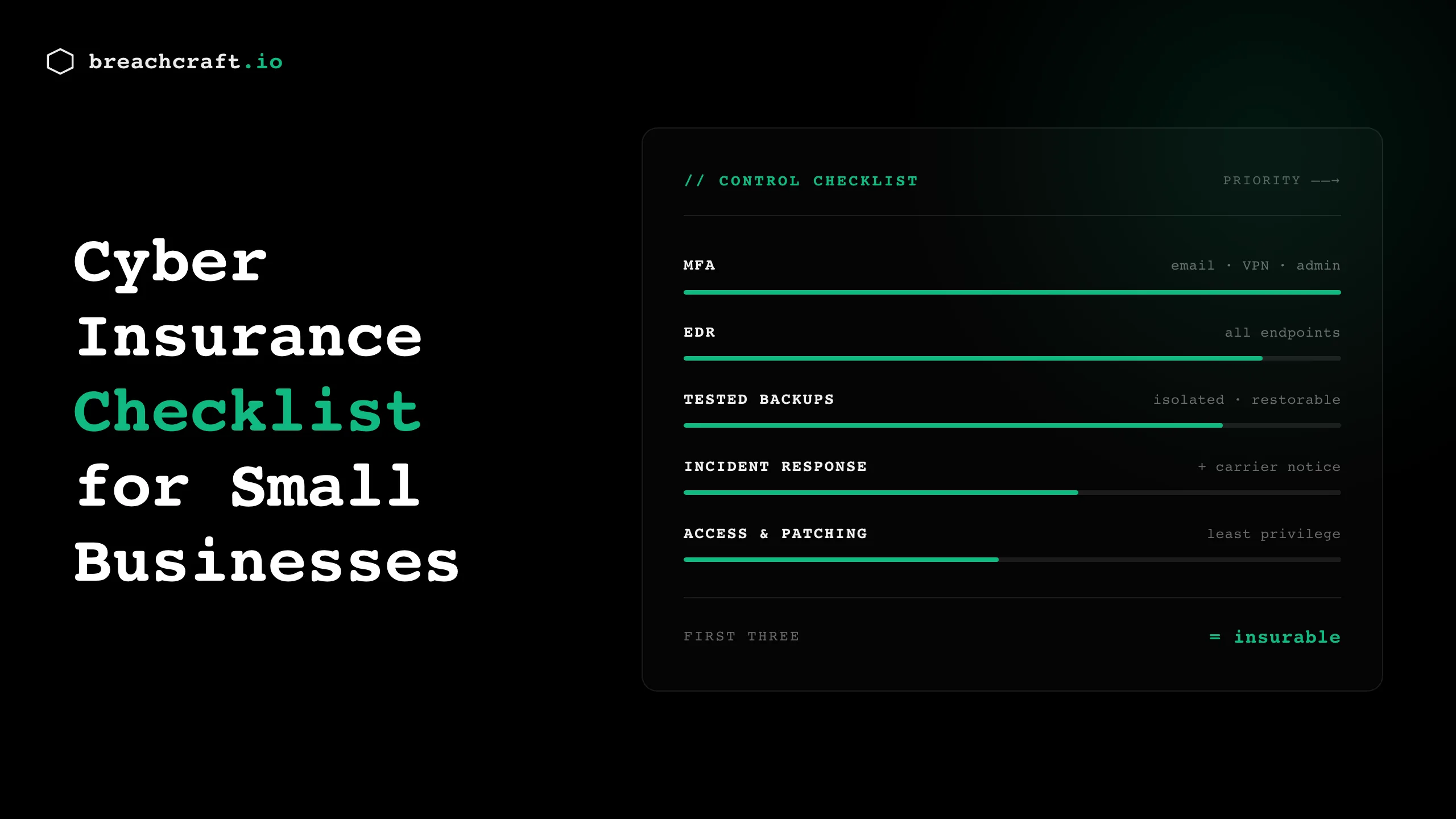

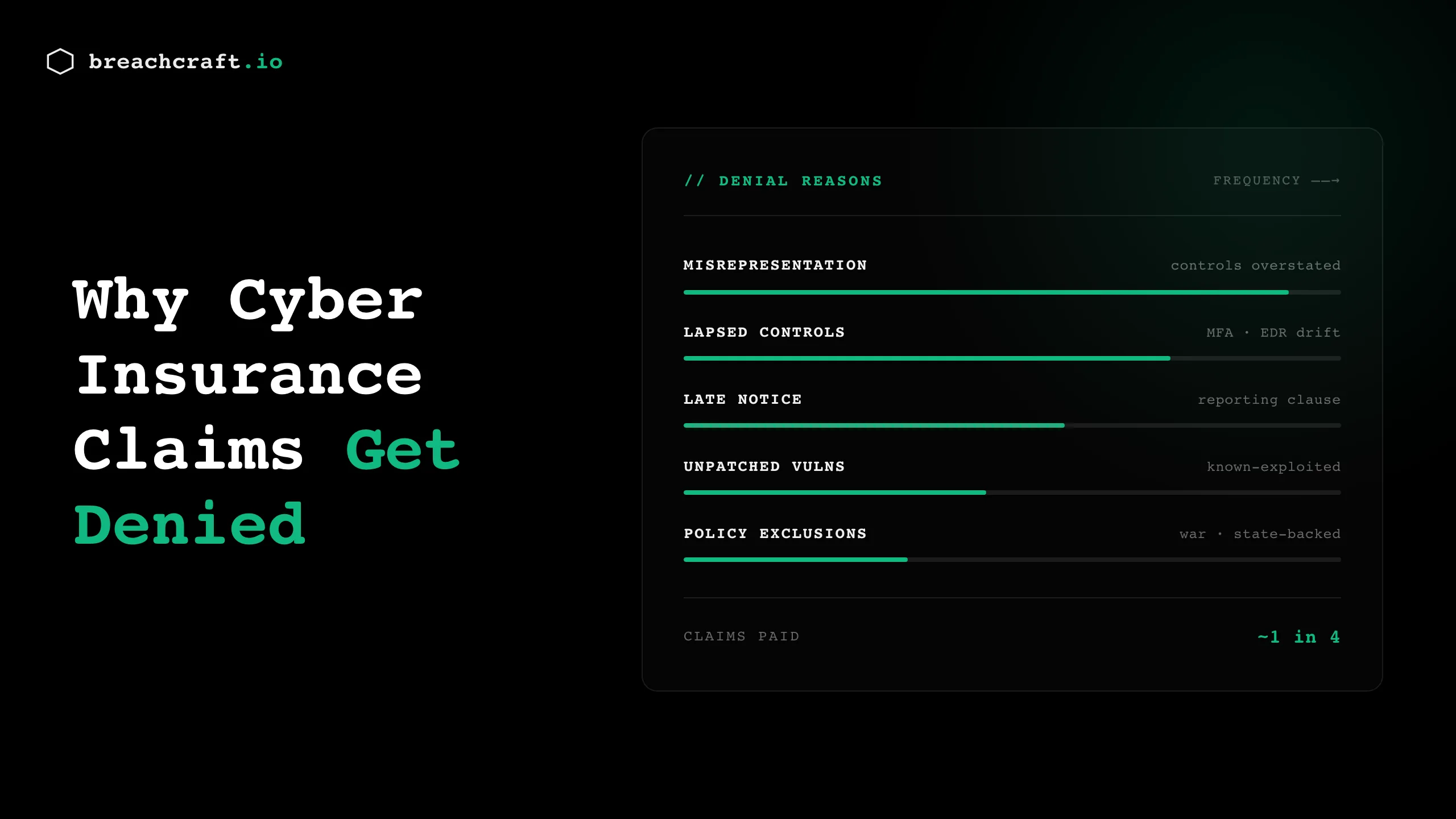

For the full picture of what carriers require before they’ll write that coverage, our cyber insurance requirements guide covers the controls side, and if you’re an SMB working toward a first policy, the cyber insurance checklist for small businesses is the place to start.

Not sure whether your coverage matches your real exposure? Contact Breach Craft and we’ll help you understand the risk your policy needs to cover.